The Hormuz Paradox: Why Markets Are Shrugging Off $110 Oil

Equities are at all-time highs. Brent Crude just broke $110. History says this disconnect has a very short shelf life.

By Ian Gross | May 4, 2026

There is a strange calm at the center of the current market storm. The S&P 500 and Nasdaq closed last week at fresh all-time highs. The VIX — Wall Street's so-called "fear gauge" — remains historically subdued. And yet Brent Crude has broken through $110 a barrel, driven by sustained friction in the Strait of Hormuz, one of the most critical chokepoints in the global energy supply chain.

Call it the Hormuz Paradox: equity markets are pricing in a world of frictionless AI-driven growth while the physical infrastructure that powers that growth is quietly becoming a geopolitical hostage.

This disconnect is not sustainable. Here is what investors need to understand before Monday's open.

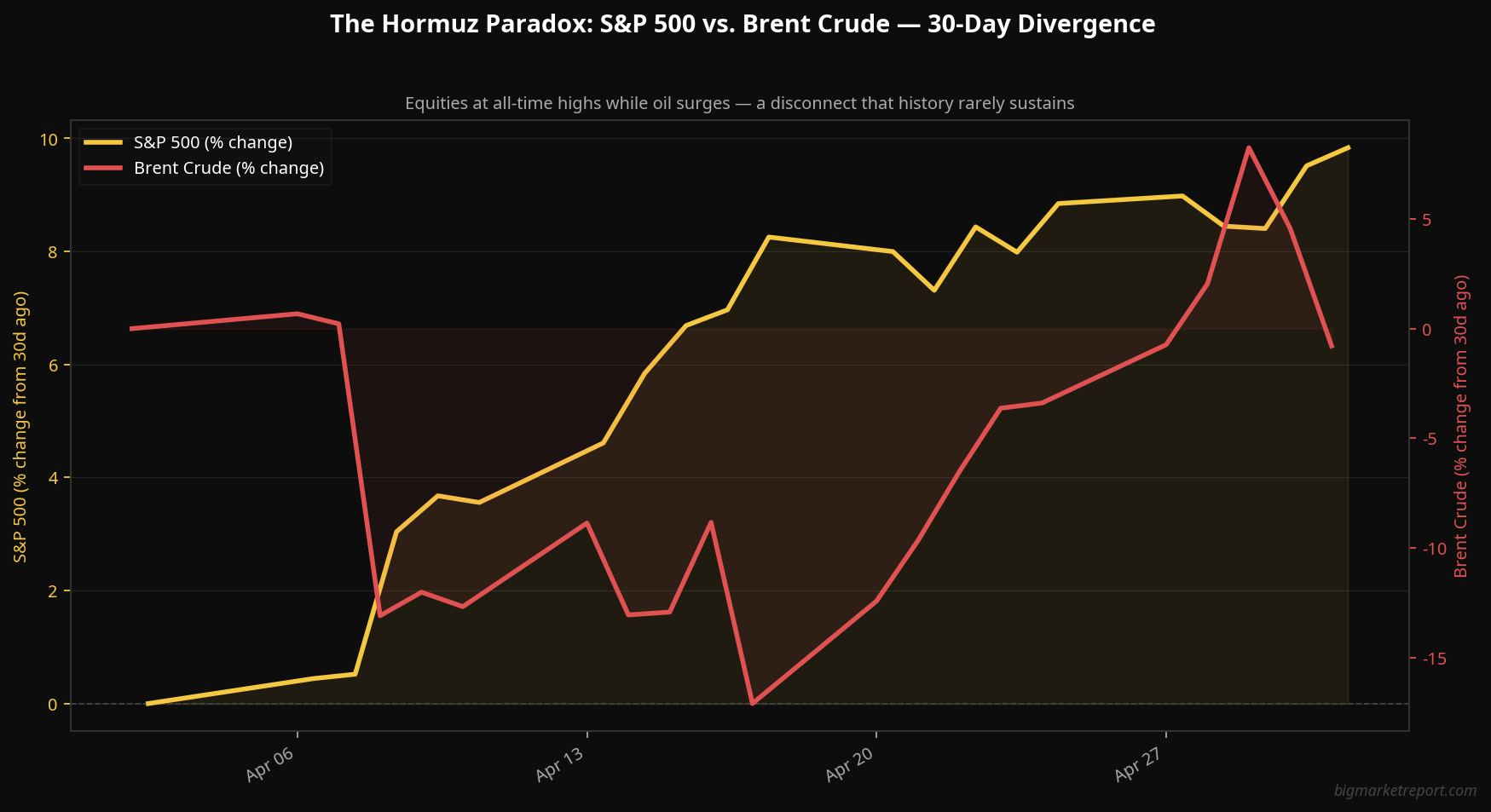

Chart: S&P 500 vs. Brent Crude — 30-day % change. Equities at all-time highs while oil surges — a disconnect that history rarely sustains. Data: Yahoo Finance.

The Inventory Buffer Has Disappeared

The conventional wisdom in energy markets is that a short-term supply disruption can be absorbed by commercial and strategic inventories. That assumption is no longer valid.

Recent guidance from ExxonMobil indicates that commercial oil inventories are at their lowest seasonal levels in five years. The Strategic Petroleum Reserve, drawn down aggressively during the 2022 energy crisis, has not been fully replenished. The cushion that allowed markets to shrug off previous Hormuz scares — 2019, 2021 — simply does not exist at the same scale today.

The Strait of Hormuz carries roughly 20% of the world's liquid petroleum. A sustained disruption is not an inflationary nudge. It is a systemic stop-block for global industrial output.

The Fed's Impossible Math

Energy prices do not exist in isolation. For the Federal Reserve, a sustained move above $110 Brent creates a policy trap with no clean exit.

The Fed's stated goal remains bringing PCE inflation back to 2%. As of the April 30 double-print, PCE was running at 3.5% year-over-year — already the highest reading since May 2023. Energy is one of the most direct pass-through mechanisms in the inflation basket. Gasoline prices, freight costs, and utility bills all respond within weeks to a sustained crude shock.

The implication is straightforward: if energy prices do not stabilize by Q3, the Fed's "higher for longer" posture is no longer a policy choice. It becomes a mathematical necessity. The market is currently pricing in at least one rate cut before year-end. That pricing is built on a soft-landing model that does not account for a permanent upward shift in the energy floor.

The risk is not just that rate cuts get delayed. The risk is that the Fed is forced to choose between fighting inflation and preventing a recession — and that there is no version of that choice that leaves equity multiples where they are today.

What to Watch This Week

Three indicators will tell us whether the market's calm is justified or complacent.

The 10-Year Treasury Yield. The 10-year is currently hovering near 4.6%. If energy fears push it through 4.7%, it will represent a meaningful tightening of financial conditions at exactly the wrong moment — when corporate earnings guidance for Q2 is still being set. Watch for a yield spike as the first signal that the bond market is pricing in what equities are not.

Energy Sector Rotation. Capital rotation into upstream oil producers — XOM, CVX, COP, EOG — is the canary in the coal mine for broader index stress. If institutional money begins moving defensively into energy while trimming tech exposure, it signals that the smart money is no longer willing to bet that AI earnings can outrun geopolitical risk.

Fed Governor Williams on Monday. Williams is one of the most influential voices on the FOMC and a reliable signal of where Chair Powell's thinking is heading. His Monday speech will be the first major Fed communication since the April 30 GDP/PCE double-print. Listen for any language around "supply-side shocks" or "energy pass-through" — either phrase would signal that the committee is actively revising its inflation trajectory upward.

The Bottom Line

Markets are making a bold bet: that corporate efficiency, AI productivity gains, and strong earnings momentum can absorb a sustained energy shock without meaningful multiple compression. It is a bet that has worked, so far, because the shock has been gradual rather than acute.

History is not encouraging on this point. The 1973 oil embargo, the 1979 Iranian Revolution, the 1990 Gulf War — each began with equity markets underpricing the duration and severity of the supply disruption. In each case, the repricing, when it came, was sharp and fast.

$110 oil is not a crisis yet. But the buffer is gone, the Fed is boxed in, and the yield curve is watching. The window for a soft landing is narrowing — and the market has not yet looked out the window.

Ian Gross is the founder of Big Media Engine and editor of The Big Market Report. This analysis is for informational purposes only and does not constitute financial advice.

Affiliate disclosure — We may earn a commission if you subscribe via the link below, at no cost to you.

Access independent analyst ratings, fair value estimates, and portfolio tools trusted by over 30 million investors. The same data institutional managers use — now available to individual investors.

Start your free trial →Ian Gross is the founder and chief editor of The Big Market Report. With over a decade of equity research, he writes analysis that cuts through the noise to explain the "why" behind every major market move.

More by Ian →Never miss an analysis